Uranium Global Market Outlook 2026

Thank you to Riko Kardamow and Potato Capital for their notes and contributions.

With all eyes on nuclear generation heading into 2026—and July 4th serving as the president’s target launch date for small modular reactors—uranium is gaining attention for its fuel enrichment properties and contributions to data center generation.

But as a commodity, how investable will uranium be this year? Together, Riko Kardamow , Potato Capital , and I will dive into its insights in the content below.

Major uranium (& nuclear) companies (NYSE) — 12-month returns:

Cameco [Canada/NYSE American] ($CCJ) – $110.20 (+125.80%, +61.39)

BWX Technologies Inc [United States] ($BWXT): $201.46 (+75.66%, +86.77)

Oklo Inc [United States] ($OKLO): $102.01 (+345.28%, +79.00)

Uranium Energy Corp [United States] ($UEC): $15.82 (+126.32%, +8.83)

Energy Fuels Inc [United States] ($UUUU): $19.58 (+8.05%, +1.40)

Denison Mines Corp [Canada/NYSE American] ($DNN): $3.40 (+77.75%, +1.49)

NexGen Energy Ltd [Canada/NYSE American] ($NXE): $11.08 (+65.37%, +4.38)

Centrus Energy Corp (American Centrifuge Operating, LLC) [United States] ($LEU): $308.90 (+342.81%, +239.14)

NuScale Power Corp [United States] ($SMR): $19.90 (+5.90%, +1.11)

Major uranium (& nuclear) ETFs (NYSE) — 12-month returns:

Global X Uranium ETF ($URA) – $54.40 (+86.43%, +25.22)

Sprott Uranium Miners ETF ($URNM): $69.57 (+62.51%, +26.76)

VanEck Uranium and Nuclear ETF ($NLR): $148.54 (+62.29%, +57.01)

Direxion Daily Uranium Industry Bull 2X Shares [2X leveraged ETF] ($URAA): $48.35 (+130.46%, +27.37)

Major uranium companies (non-NYSE):

China General Nuclear Power Corp [China] ($CGN)

The largest nuclear power operator (as of 2024) has more than 50% of the market’s nuclear power in operation. World’s largest nuclear power construction company.

Kazatomprom JSC GDR [Kazakhstan]

Orano [France]

Uranium One [Russia]

High Assay, Low Enriched Uranium (HALEU) companies — 12-month returns:

Centrus Energy Corp (American Centrifuge Operating, LLC) [United States] ($LEU): $308.90 (+342.81%, +239.14)

General Matter [United States]: not publicly traded

Louisiana Energy Services [United States]: not publicly traded

Orano Federal Services [United States]: not publicly traded

Largest uranium producers (2024):

Kazakhstan – 23,270 tons (39% of world supply)

Canada – 14,309 tons (24%)

Namibia – 7,333 tons (12%)

Australia – 4,598 tons

Uzbekistan – 4,000 tons

Russia – 2,738 tons

China – 1,600 tons

12. United States – 260 tons

1. Supply-Demand Balance

In 2025, uranium demand–but also supply–was defined by policy uncertainty. The United States’ tariffs on exporting countries initially paused trade with some of the country’s primary energy trade partners, including Canada and Mexico, which each received various threats of a 25-50% tariff (with only a 10% tariff applied to energy and potash). The United States purchased uranium from the following countries in 2022:

Canada (27%)

Kazakhstan (25%)

Russia (12%)

Uzbekistan (11%)

Australia (9%)

Six other countries (16%)

And only 0.2 million (~0.5%) of the 36.7 million total tons of uranium from US nuclear power plants came from domestic concentrate production that year, meaning that uranium use (and subsequent nuclear generation) was dependent on international trade—primarily with Canada, one of the countries that received the inaugural round of tariffs. In the midst of its ongoing sanctions to end the Russia-Ukraine war, the United States is also shifting its uranium exports away from Russia.

As a result, Western companies have been less certain about whether to continue increasing development, despite also understanding the critical contribution that uranium would make to nuclear energy generation. The 29th Conference of the Parties (COP29) saw 31 countries commit to tripling their nuclear energy capacity by the year 2050, which symbolized the growing demand for both nuclear energy and uranium. This commitment expanded on President Biden’s pledge for the United States to do the same in COP28. However, verbal commitments to increasing production aren’t tangible production, and near-term supply capacities still aren’t expected to meet the level of exponential demand growth in the next few years. This is bullish for uranium’s forward curve, even as the spot price of triuranium octoxide (yellowcake / U3O8) hovers around a high $85 per pound.

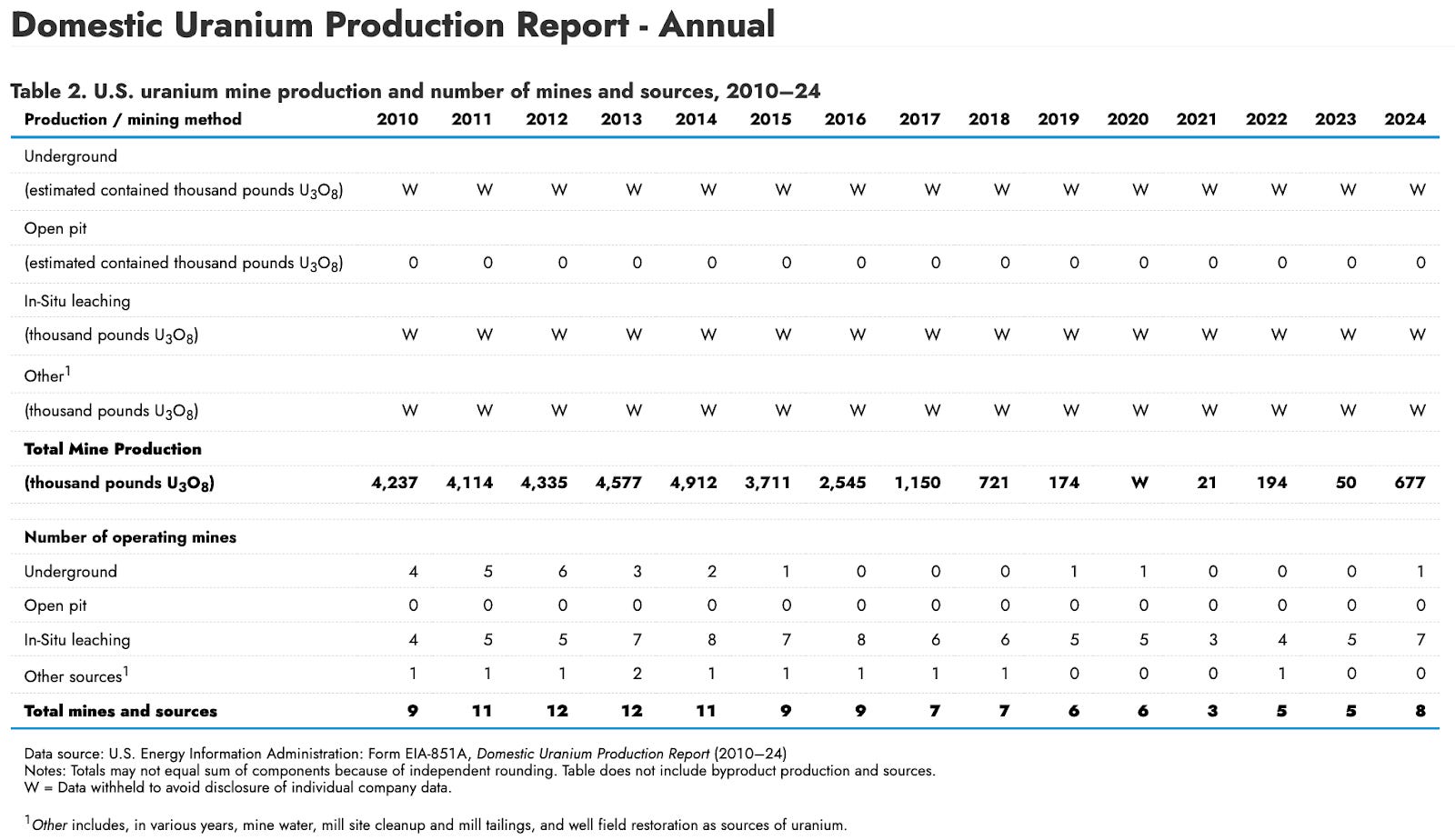

But while the United States mines only domestically produced a small percentage (under 1%) of its total power plant uranium fuel in 2022, US production has skyrocketed since then. In 2024, United States uranium mines developed 677,000 pounds of yellowcake uranium (with seven In-Situ leaching mines in operation), which is up from only 50,000 pounds in 2023 (and 194,000 pounds in 2022):

The seven In-Situ Recovery (ISR) facilities included the Alta Mesa Project, Rosita Project, Lost Creek Project, Smith Ranch-Highland Operation, Ross Central Processing Project, and Willow Creek Project in South Dakota, Texas, and Wyoming (EIA), which operated with 14.1M pounds of U3O8 of capacity per year in 2024. Employment in the US’ uranium production industry also rose by 49%, with 506 full-time employees in 2024 from 340 in 2023. Domestic production is growing, and while supply won’t be substantial enough to support nuclear production independently of international imports for a number of years, it is a clear signal that demand growth is real and that uranium is worth the infrastructure investments.

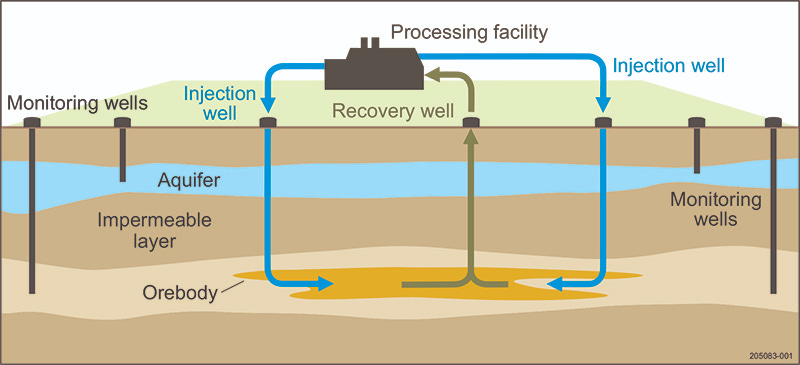

In-Situ mining was mentioned in the last paragraph—what is this? Uranium isn’t a rare earth metal, but it is a common byproduct of rare earth mining, as it is found close to the crust of the Earth and can be drawn out of rare earth deposits. There are two common forms of mining for uranium:

In-Situ Recovery (ISR) / Solution Mining (most popular method)

Recovery mines will pump lixiviant (chemical-water mining solution) through a series of grid-placed injection wells, which push the uranium ore-liquid up through a central tube to a recovery well.

This mining method has become more commonly used for its ability to efficiently mine ore without permanently harming the surrounding land (for farming and cattle).

First introduced in the 1970s and used in the United States, Kazakhstan, China, Russia, and Australia primarily for potash, salt, uranium, and copper.

Conventional Mining (Open Cut Pit & Underground)

Large pits are dug to remove overburden, and uranium ore is mined in large chunks in a more traditional extraction method (crushing and leaching the ore to extract the uranium).

Much more dangerous, wasteful, and environmentally unfriendly than In-Situ, but has the potential to uncover more ore (that wouldn’t be reached with the injection wells).

There were three conventional uranium mines operating in Texas through 1972-1989, but they have since been deactivated.

The Nuclear Regulatory Commission becomes involved as soon as the uranium ore is processed (chemically altered), or once the ore arrives at the conventional mining mill or ISR facility. The NRC regulates ISR facilities and mills (currently in New Mexico and Nebraska), but doesn’t regulate conventional mines—state agencies regulate recovery operations in Colorado, Utah, Texas, and Wyoming (NRC.gov).

In 2025, uranium demand–but also supply–was defined by policy uncertainty. Insufficient investments in new capacity in 2010’s has hampered utilities in their abilities to put forward new nuclear construction in the 2020’s, especially as small modular nuclear reactors (SMNRs) grow in popularity for their efficiency, safety, and flexible transportation. However, with data centers (for the purpose of supporting artificial intelligence technology) now accounting for as much as 10% of the country’s total load by 2030, nuclear development is being streamlined as a necessity. And President Trump is recognizing this necessity, as the Trump administration and US government just recently reported that ~$80B of new reactors (not just previously-decommissioned reactors) will be invested in the near future. Maybe most importantly, there are no current US tariffs on the uranium trade and international exports in 2026. Tariffs

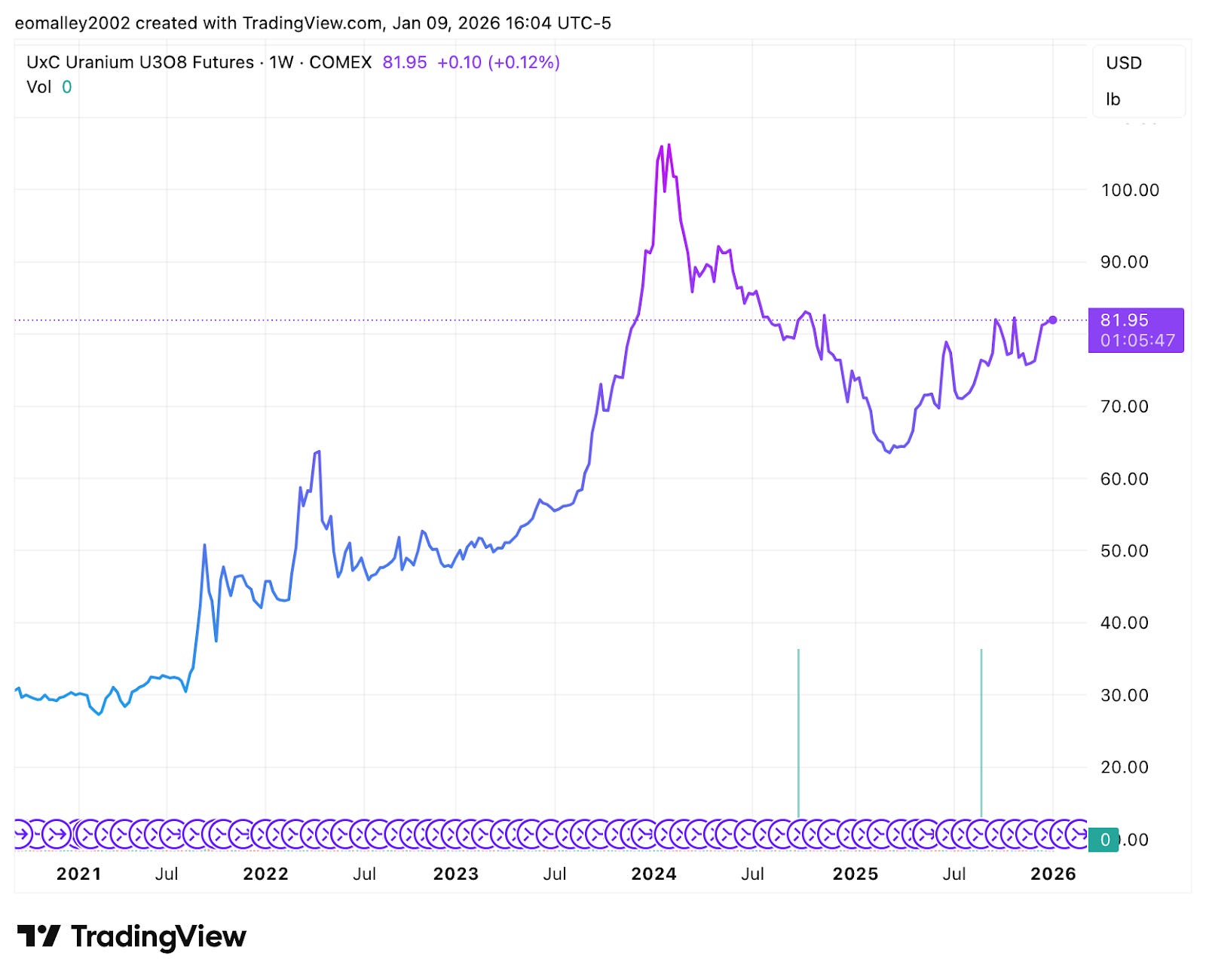

2. Uranium Prices (bullish spot price)

Unlike other commodities, uranium is traded privately and isn’t available on the open market. The spot price for uranium has risen to $81.95 per pound at the time of this article (1/9), which is credited to high long-term demand and slashed regulations on uranium converter permitting—. The Trump administration is pushing for accelerated mining and development in the uranium and nuclear space (working with the NRC to remove restrictive testing regulations on nuclear projects).

Looking at the largest peaks in U3O8’s trading history:

June 2007: Uranium Bubble: peak price of $136 per pound

The Cigar Lake mine (Saskatchewan, Canada) flooded. This delayed access (and supply) to one of the largest uranium deposits in the world.

January 2011: peak price of $72.63 per pound

Nuclear optimism before three Fukushima Daiichi nuclear reactors were melted down in an major earthquake in Japan (which took the lives of +15,000 people). On an upward trend until early 2011, uranium prices began to tank for the next decade after nuclear safety concerns began to outweigh generation potential.

March 2022: peak price of $58.20 per pound

Russia-Ukraine supply shocks. Energy prices in general spiked at the start of the war due to Russia’s high oil and natural gas reserves, but for uranium as well, due to the United States’ high reliance on low-enriched uranium exports from Russia.

January 2024: peak price of $100.25 (first time breaking $100 since 2007)

Kazatomprom (Kazakhstan) plants faced shortages of sulfuric acid, which is a major contributor to uranium production (and the extraction process). Kazatomprom is the largest uranium producer in the world (with an expected 25,000-26,500 tons per year of production in 2025).

Most of the above price spikes resulted in a shortage of supply, rather than an influx of demand. In 2026, uranium demand is expected to continue surging, even as supply (and US production) continues to grow. The United States Department of Energy announced that it will give $2.7B to American Centrifuge Operating, General Matter, and Orano Federal Services for High Assay, Low Enriched Uranium (HALEU) enrichment development on 1/5/26, with only Russia currently producing HALEU at a commercial level (and the US banning uranium imports from Russia by 2028). The enrichment of uranium (processing the substance to 5-20% U-235 — required for creating a more reactive fuel) is specifically necessary for SMRs, and this development is supporting the demand for both new electricity load and new power generation.

The Bifurcation of Utility Procurement Strategies

The prevailing market consensus is currently paralyzed by a fundamental misconception: an obsessive tracking of spot uranium fluctuations as if they still reflect the true equilibrium of the sector. This is a classic instance of reflexivity based on imperfect knowledge; while retail capital chases the noise of daily liquidity, they are blind to a violent structural decoupling occurring in the real economy. The driving force is a new, price-inelastic variable—the hyperscalers—who view baseload power not as a line item, but as an existential requisite for AI infrastructure, forcing a bifurcation of the market into a legacy wholesale tier and a premium, security-first tier.

This transition creates a profound asymmetry for the average investor, as utilities act as intermediaries to wrap North American producers in the superior credit profiles of these tech giants. Specifically, the market is seeing contract durations extend well beyond a decade with hard floors exceeding $75/pound. Consequently, the trade for 2026 is no longer a speculation on commodity beta, but a recognition that these producers are undergoing a metamorphosis from volatile miners into de-risked infrastructure assets, and this valuation gap must be exploited before the broader market corrects its false narrative.

3. Reactor Pipeline & Nuclear Capacity

As of a White House executive order from May 2025, the Trump administration planned to deploy 300 GW of new nuclear capacity by 2050, with over ten (new) large conventional reactors in the construction process by 2030. With the United States in a state of national energy emergency since Trump stepped into office, the strict environmental and safety regulations have prolonged new development in these uncertain areas have been lifted, as new generation is prioritized. Whether or not the accelerated review process is beneficial to environmental protection, it will certainly assist in bringing fast development online.

“America is facing an alarming energy emergency because of the prior administration’s Climate Extremist policies. President Trump and his administration are responding with speed and strength to solve this crisis. The expedited mining project review represents exactly the kind of decisive action we need to secure our energy future. By cutting needless delays, we’re supporting good-paying American jobs while strengthening our national security and putting the country on a path to true energy independence.” — Secretary of the Interior Doug Burgum

The United States Department of Energy recently announced that it will give $2.7 billion to American Centrifuge Operating, General Matter, and Orano Federal Services for High Assay, Low Enriched Uranium (HALEU) enrichment development on 1/5/26, with only Russia currently producing HALEU at a commercial level (and the US banning uranium imports from Russia by 2028). The enrichment of uranium (processing the substance to 5-20% U-235 — required for creating a more reactive fuel) is specifically necessary for SMNRs, and this development is supporting the demand for both new electricity load and new power generation.

However, the unspoken skepticism of these investments still speaks loudly—what will happen once Trump and his anti-climate change stance leave office? Will the next administrations continue advancing nuclear investments and minimizing permitting restrictions in the same capacity? We witnessed how quickly the clean energy subsidies from President Biden’s Inflation Reduction Act were cut off early last year—even these could be brought back in just three years.

The most recent large conventional nuclear power plants to start commercial operation were the Vogtle units 3 & 4 in Georgia, which drew criticism for taking more than double the expected time and total cost to build the plants: 13 years (2011-2024) and $36.8 billion. Requiring a project timeline of 10+ years is extremely risky for developers who previously had little incentive to take on such a massive deal without the certainty of completion and investment return.

Granted, these were the first large conventional plants to be built in over 30 years and faced a series of complications, including COVID, supply chain disruptions, new reactor designs, and the bankruptcy of project partner Westinghouse Electric Company, LLC (due to the cost hikes and construction interruptions incurred from Vogtle).

The downfall of Westinghouse nearly took down Toshiba, which purchased Westinghouse in 2006 and had to sell its stake in Brookfield Business Partners in 2018 (exiting the nuclear industry completely). Westinghouse is now jointly owned by Brookfield (51%) and Cameco (49%) as of 2023. Toshiba’s reputation is still recovering from the construction of the Vogtle units and the Fukushima Daiichi reactor meltdowns (prompted primarily by the tsunami, but still holding the nuclear operators liable).

However, it is arguable that trial-and-error projects like Vogtle laid the necessary foundation for developers to take initiative on building future large conventional plants. The AP1000 reactors used in Vogtle 3 & 4 are also currently operating in China (16 total)—Westinghouse approved four new AP1000 reactors to be built as part of the Bailong Nuclear Power Project in Guangxi Province with China’s State Power Investment Corporation (SPIC) and China General Nuclear Power Corporation (CGN) in August 2024—and have modern advanced cooling systems and the lowest carbon footprint (8.4 g CO2e / kWh) of existing reactors (even including some SMRs).

According to a PwC presentation on Westinghouse’s AP1000 project proposal in Ontario, Canada (four new AP1000 pressurized water reactor units), the development could bring:

$28.7 billion of GDP ($1.79 billion per year) and 126,560 person-years of employment through 4,800 MW of nuclear capacity.

$15,690 million of labor income.

Generation for +750,000 homes annually (per unit).

Contribution to Canada’s 2030 emission reduction plan.

Over a 16-year manufacturing and full-installation time period.

AP1000 reactors are also being approved in Poland, Ukraine, and Bulgaria, while still being considered in the United Kingdom, India, Canada, and the United States.

China saw a 48% decrease in construction timeline for its second series of AP1000 projects (Sanmen 3 & 4, Haiyang 3 & 4), with Sanmen Nuclear Power Station’s Units 3 & 4 first approved for construction in April 2021 and projected to come online to the grid in 2027-2028—around 6-7 total years. This reduction in time, while not yet possible in the United States (as China’s nuclear fleet and infrastructure are significantly more developed), is promising to the United States’ expansion, as it may signal that the delays halting the Vogtle construction may be solved with additional building experience.

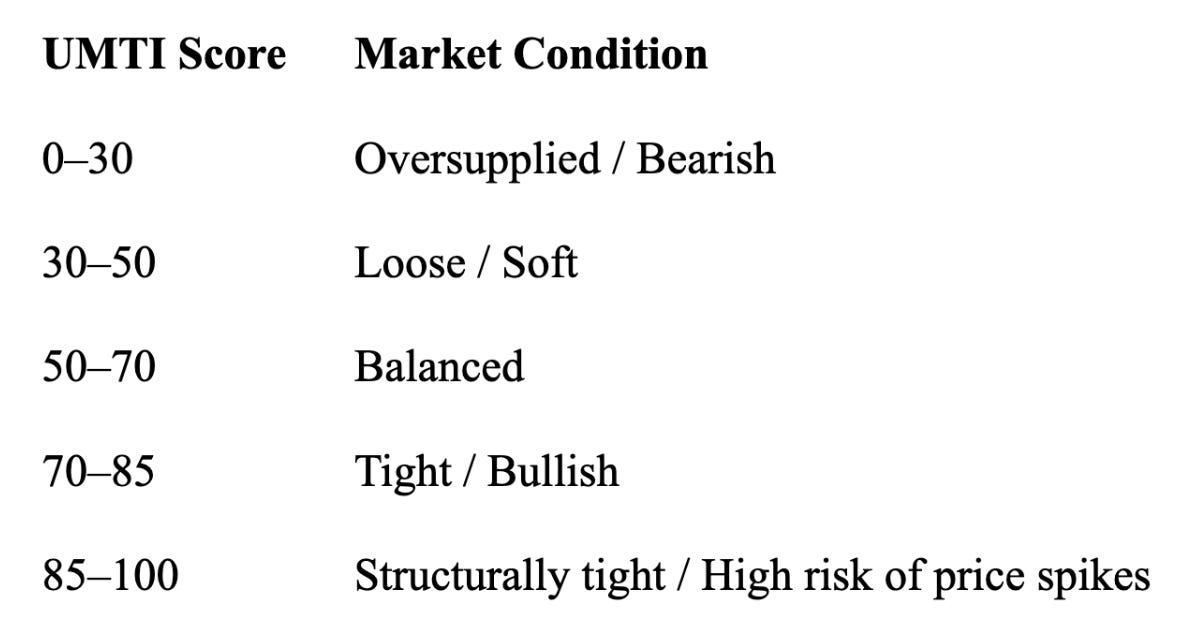

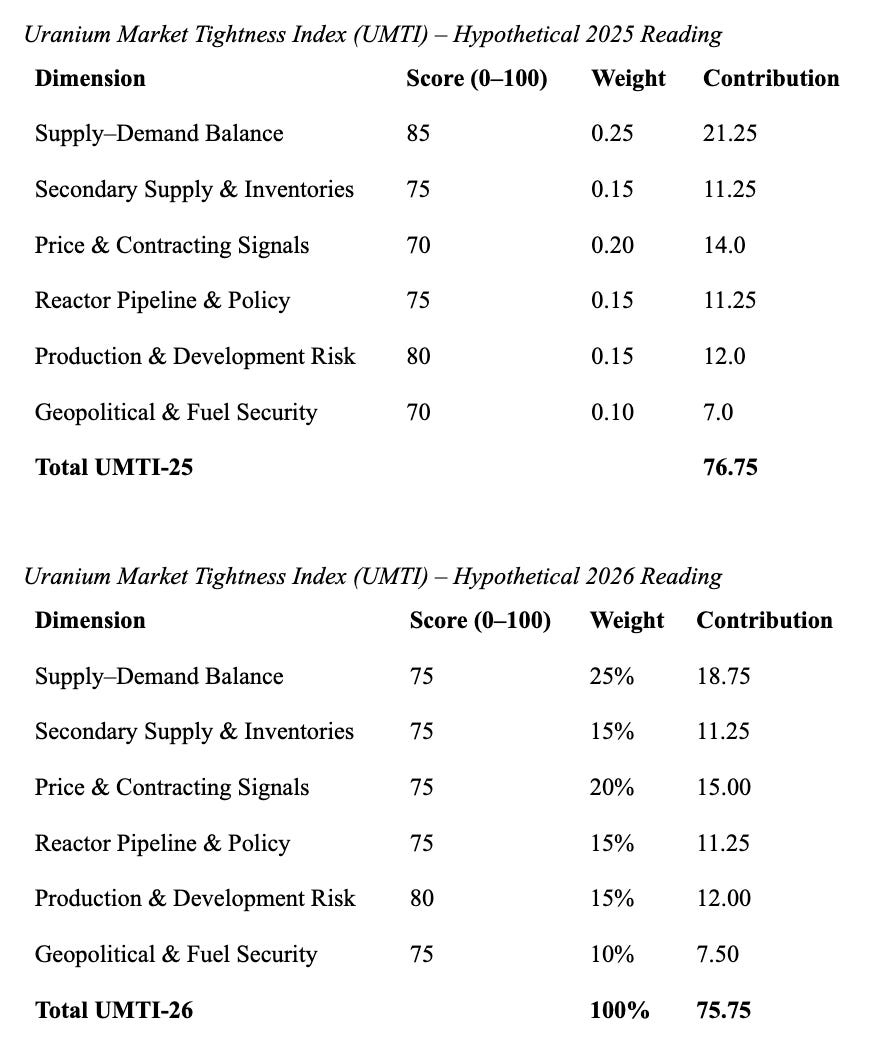

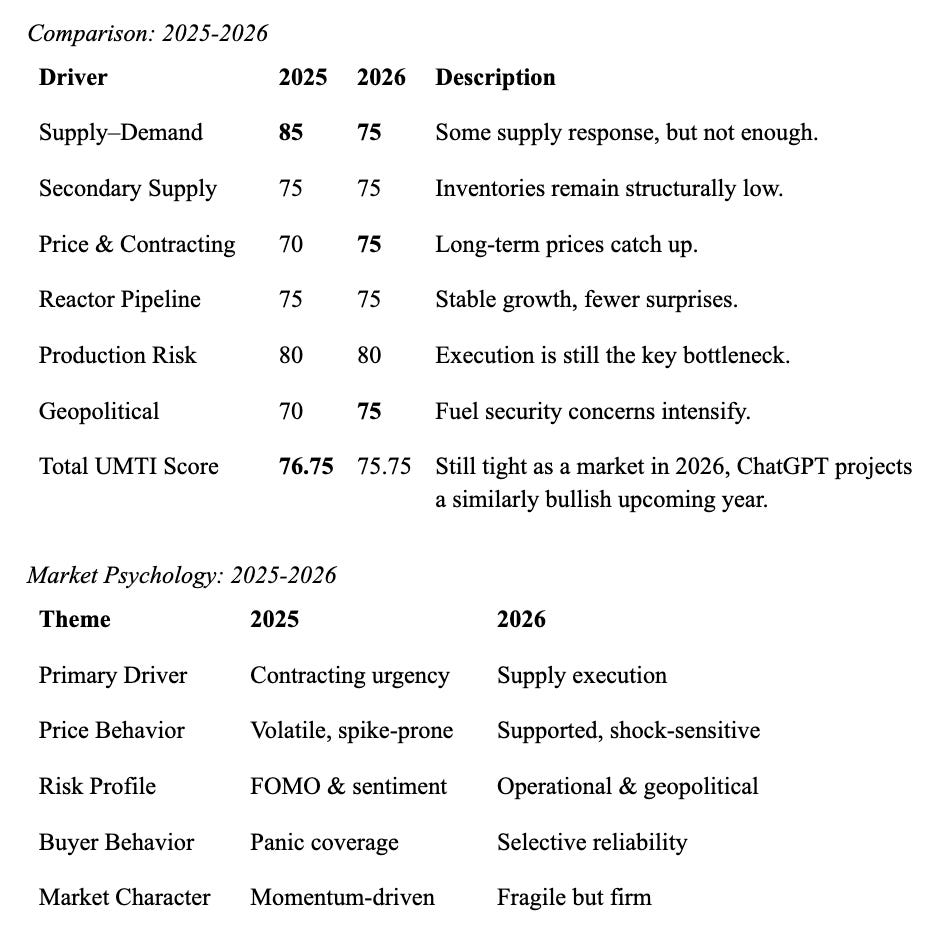

4. Market Tightness Indicators

To analyze the liquidity of the uranium commodity market in 2026, I asked ChatGPT to create the following index (measuring the weight of important supply & demand indicators).

UMTI = ∑(Scorei × Weighti)

Where weights are decimals (e.g., 25% = 0.25).

This index calculation was run for the 2025 and 2026 calendar years, with indicator categories split up to provide a holistic “score” to measure the investible nature of uranium in each time period. An explanation of the score’s rating system is provided below:

ChatGPT predicted that the uranium market will remain constricted by thin supply shortages in 2026, but will offer more a consistent spot price as a “fragile but firm” market character lifts the rate higher, as months of stagnation preceded the slight hike.

As John Ciampaglia (CEO of Sprott Asset Management LP) states, tariff and policy uncertainty have defined uranium’s year in 2025, as many other energy commodities have experienced, but these risks are largely in the rear-view mirror due to President Trump’s exemption of tariffs from uranium trade.

Final Thoughts

Investors are bullish on uranium heading into the new year, including the uranium producers (Cameco, Energy Fuels Inc., enCore Energy Corp., Ur-Energy) and long-term pricing. Utilities are the biggest purchasers of uranium, and although they have been falling behind in procurement, demand growth for new nuclear projects is expected to carry positive momentum forward for investors.

While the supply chain for building large conventional reactors has been severely depleted since the 1970s (and compared to more advanced countries like China), the United States is quickly ramping up its infrastructure to build economies of scale—mostly with SMRs, which will theoretically be produced in mass quantities in the coming years (Oklo, NuScale Power).

The Trump administration and Department of Energy Secretary Chris Wright have acknowledged these primary concerns and are working on correcting them, particularly through the DOE’s Nuclear Reactor Pilot Program, which will aim for the construction and operation of (at least) three test SMRs by July 4th, 2026. Advancements and licensing fast-tracks like these will push ahead for nuclear development, which will in turn advance uranium demand.

It’s an exciting time to analyze uranium, and changes in 2026 will undoubtedly shape the nuclear development landscape for decades to come.

| A guest post by

|

| A guest post by

|